We're building something new – take a look at the beta site: intglobal.com

Choose the right premium, build the right marketing campaign and elevate the value! – insurers are facing challenges maintaining a balance between providing enhanced customer experience and operating at the profit margin. When we talk about the underwriting process and the traditional method, we can see much human intervention and manual paperwork. It can only make the process gruesome!

Reports suggest that the key challenges insurance companies face are binding the data and advanced technological capabilities into one to build value in the Insurance Value Chain. A formation of a successful strategy occurs when insurers can identify the business value generated by the ML and how it can be aligned across the business domain.

Solutioning to this challenge, today, insurers are joining hands with software development partners to bring a radical change in the sector through early adoption. When we talk about the insurance value chain, we understand the end-to-end process from product development to underwriting and claim processing.

As ML is an integral part of data science, so is underwriting for insurance. The ongoing crisis has reinforced the urgency to modernise the underwriting process. The companies that are adopting end to end digitisation of the underwriting process are the ones that are overcoming slowing down factors and modernising the customer journey in the underwriting process. Let us see how the analytics can be leveraged in the underwriting process from reporting to binding policy:

Descriptive analytics: Claims are deeply studied and patterns are identified. Based on past historical data, descriptive analytics flags if any new trends emerge.

Predictive analytics: As the process moves, underwriters use predictive analytics to evaluate the pricing competitiveness. It also alerts the underwriter through its risk scoring and assessing model.

Prescriptive analytics: Further underwriter deploys prescriptive analytics to build a model based on the future economic scenario and predicts the future risk of the policies. It applies the advanced statistical model to recommend solutions such as automated underwriting in case of the most predictable risks.

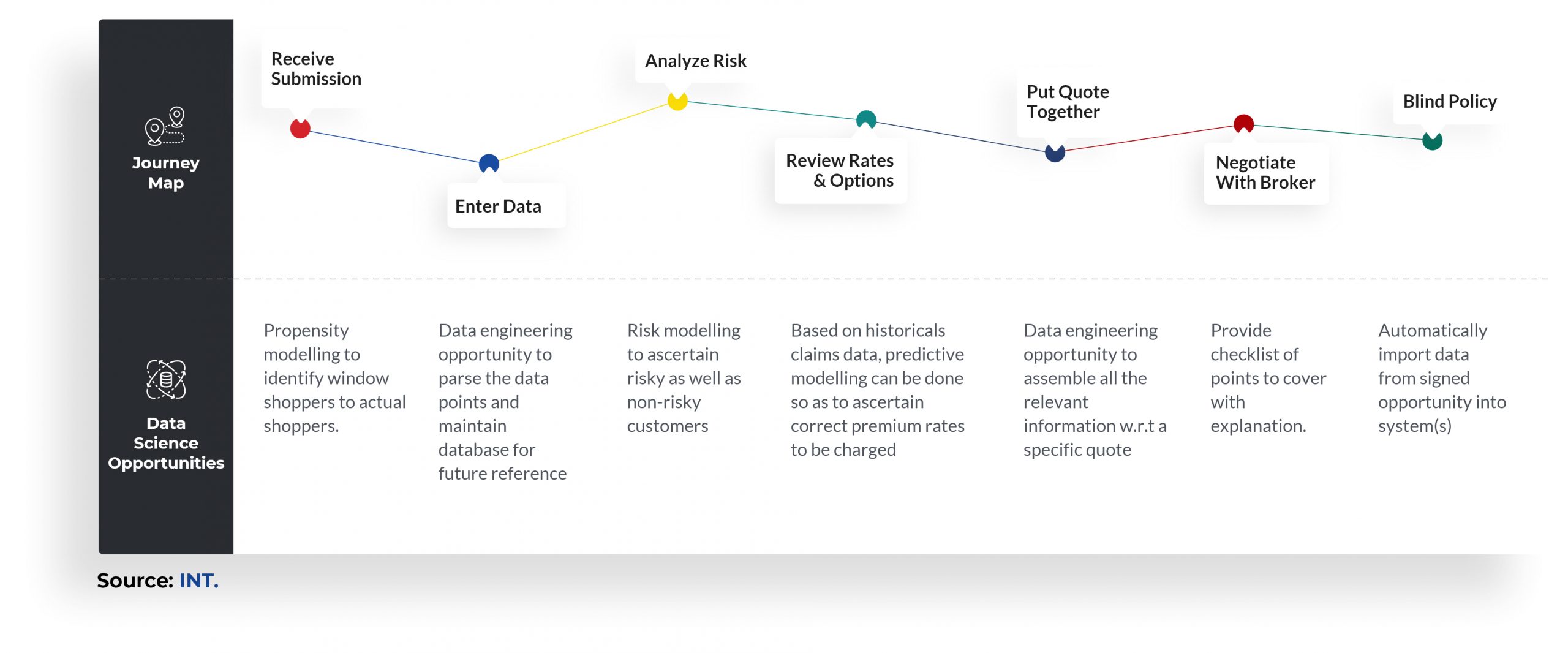

Recently machine learning is leveraged in the underwriting process, thus we have deeply studied the customer journey in the underwriting process to understand how it has improved and provided a seamless experience. Based on it, we have allotted the data science model, which can be leveraged by the insurers to effectively understand the journey and use it to the advantage of it.

Submitting the TIFF/JPEG format form: When insurers confirm about digitally submitting the claim documents, they mean they are submitting image format documents. Data scientist deploys tools and models to parse the data and build a structured form.

Analysing the risk: It becomes essential for the underwriter to get a granular view of the risk based on the historical risk and cost drivers. Underwriters are deploying a machine learning model. Based on the data generated from the social media platforms, historical data, and data from a third-party platform, the model assesses and scores the risk accordingly. Also, the classification model segments the customers based on their likings, motivation to purchase, etc., which further helps evaluate the risk and quote the premium well.

Reviewing Rates and options: The rates depend upon the actuaries, and actuaries rely on the risk scoring model. Predictive analytics plays a more significant role when quoting the premium. Collection of the correct data, such as the likelihood of rash driving, sickness, defaulting, and other external data sources, are essential for the risk assessment. After the evaluation, if the underwriters find that the claim outcome is within the risk parameters, underwriters can easily quote the premium without much complexity. Through predictive analytics, underwriters are empowered with confidence due to certainty of risk.

To minimise the underwriting risk, there should be well-defined risk parameters by the underwriters. Predictive analytics is providing statistical reliability and a stable rule-based method for improving pricing decisions. It is also helping insurance companies to perform well at the margin during adverse underwriting environments and at INT. we provide end to end guidance so that our partners effectively manage the dashboard and use the analytics built on an advanced technological model. Book us for the demo!