We're building something new – take a look at the beta site: intglobal.com

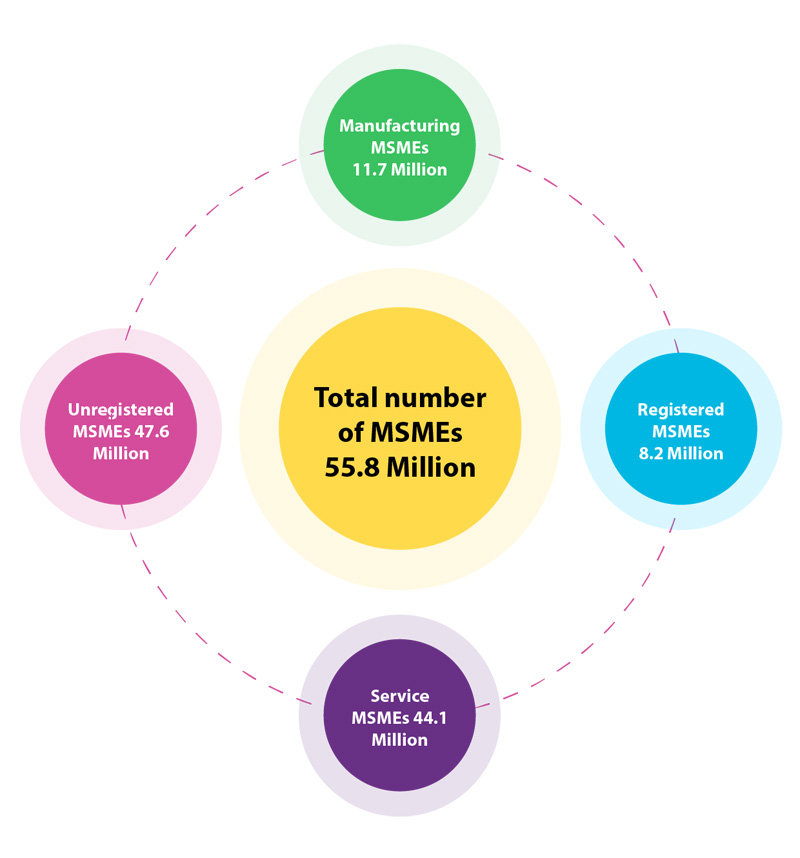

Snapshot of the current Indian MSME sector

Source: MSME Annual Report

Source: MSME Annual report

Traditional Financial institutions remain wary from providing loans because

The overall demand for both debt and equity finance by MSMEs is estimated to be INR 87.7 trillion (USD 1.4 trillion), which comprises INR 69.3 trillion (USD 1.1 trillion) of debt demand and INR 18.4 trillion (USD 283 billion) of equity demand.

This need for technology disruption in formal debt financing has been underscored by a credit gap – estimated at USD230 billion in 2017 – coupled with demand and supply-side issues in financing for MSMEs.

Source: Estimation-of-Debt-Requireme-nt-of-MSMEs-in_India report

The Role of Technology in Driving Digital Finance

According to PWC, MSME banking is likely to be the fourth-largest sector to be “disrupted” by Fintech in the next five years after consumer banking, payments, and investment/ wealth management.

Fintech companies are offering solutions that can substantially improve efficiencies at every step of the lending process. Fintech models can provide end-to-end solutions for the lending value chain or “full stack lending models” such as peer-to-peer (P2P) lending, marketplace lending, crowdfunding, invoice based financing and so forth. Currently, a number of Fintech companies are providing for small-ticket loans focused on MSMEs that have limited credit history and need formal funding.

How are incumbents using Fintech solutions for digital lending?

The advent of digital lending has addressed some of the major customer on-boarding hurdles faced by loan seekers in India. Kotak Mahindra Bank which launched its flagship Fintech product Kotak 811 to offer instant credit card issuance states that there was an 85% customer opt-in for the free credit score assessment.

In addition to retail credit offerings to individuals, lending startups can play a vital role in formalising credit delivery to MSME, where 40% of the borrowing is still being carried out through informal channels and cash transactions.

Bengaluru-based Shubh Loans has started the process to apply for an NBFC licence. The platform, founded by former banker Monish Anand and Goldman Sachs executive Rahul Sekar, is targeting the financially underserved segment. Shubh Loans has reached a monthly disbursal rate of INR 15 crore and is doing around 5,000 loans per month.

Another tech startup Moneytap had begun by offering a credit line to consumers in partnership with private sector lender RBL Bank. The Moneytap app was launched in 2015 with RBL Bank, that lets lenders procure a sum between INR 3,000 to INR 5 lakh at a lower interest rate than incumbents. Once the amount has been payed-off, the app let its lender apply for more sum.

Way Forward

The future of Financial Services industry is bound to be customer-centric, technologically up-to-date( driven by the world of digital) and supportive of internal and external innovation efforts.

According to PWC, more than 90 percent of MSME digital borrowers in the next five years will be first-timers. Consequently, there will be more drop-offs as MSMEs become frustrated or confused by the journey and abandon their efforts. Roughly 30 percent of MSME borrowers expressed increased comfort with digital lending when assisted. It is critical for lenders to support these customers through call centres and chat messengers.

Emerging technologies companies need to take a new approach and ease customer journey. Moreover, partnering with digital enabler companies to put together skills and learnings can help them to make use of modern cloud-based or open-source systems utilised by FinTech companies, and they should work together to integrate new technologies in already existing architecture. Successful partnerships between Fintechs and traditional financial institutions could be a game changer for MSME lending in India: