We're building something new – take a look at the beta site: intglobal.com

Investing our hard-earned money is always risky. In fact, any sort of investment and asset allocation is complicated. And with thousands of investment plans and advice openly floating in the market, we often end up spending a huge amount of time thinking where we should invest. We also worry constantly about how we should go about the financial planning depending on the market dynamics.

The arrival of robo-advisors disrupted the traditional fintech sector and changed the way investment models worked so far. Though the term, robo-advisor nearly is nine-years-old, these so-called online wealth managers are increasingly becoming popular in the FinTech services and are building the portfolio for the investors according to their personal needs.

What are robo-advisors?

In simplest terms, robo-advisors are computer programs who invest money for the clients in the market. Investors will be asked certain questions about their investment plans, time period and risk tolerance. Robo-advisors using machine learning, big data, and algorithms will manage an ETF (exchange-traded fund) portfolio that best suits the need of the investors online with little or no human intervention. Also, when and how the market moves, the robo-advisors will adjust the portfolio of the client.

Interestingly, it was during 1998, the year of Great Recession, when Betterment unveiled to the world the financial innovation, called robo-advisor. And within a few years, these automated investment platforms driven by artificial intelligence, are one of the developing innovations in the FinTech sector. As indicated by consulting firm AT Kearney, assets under management (AUM) by robo-advisors will take a leap by 68% annually to a gigantic 2.2 trillion in the coming five years.

Robo-advisors have evolved into three distinct models with all sharing the same goal.

Interestingly more firms, dealing with finance, insurance, wealth management and investment gradually understand the disruptive potential of this new innovation and are either buying, building or partnering with robo advisory firms. Now, for the online brokers, who were once-upon-a-time stock brokers, before the Internet revolution completely changed the way finance services were handled, robo advising looks more or less of an electronic service for them.

Having said that, traditional companies shouldn’t rush and shift to digital technology suddenly. Reason? Well, let’s not forget they have a number of aging investors who prefer to take decisions from a human advisor till now. In short: at times, they prefer the human touch more than digital. Those firms need to educate the elderly clients about digital platforms and their advantages. This will reduce human liability to manage clients on a day-to-day basis and focus on expansion.

Also, it’s important to understand that robo-advisors periodically review recommended portfolios. So, if there is any change in funds or new funds are added, robo-advisors provide relevant reasons for you to decide whether or not to make any changes in your portfolio. It is important to note that most automated platforms are structured around long-term investments with little or no human intervention in recommended products.

But what do you do in short-term investments? In short-term investments, market volatility or in cases of personal emergencies, the automated advisory platform at the most sends the clients’ reminders that he/she is deviating from the long-term goals. However, cash flow and behaviour management suggestions are only offered by full-service robo-advisors.

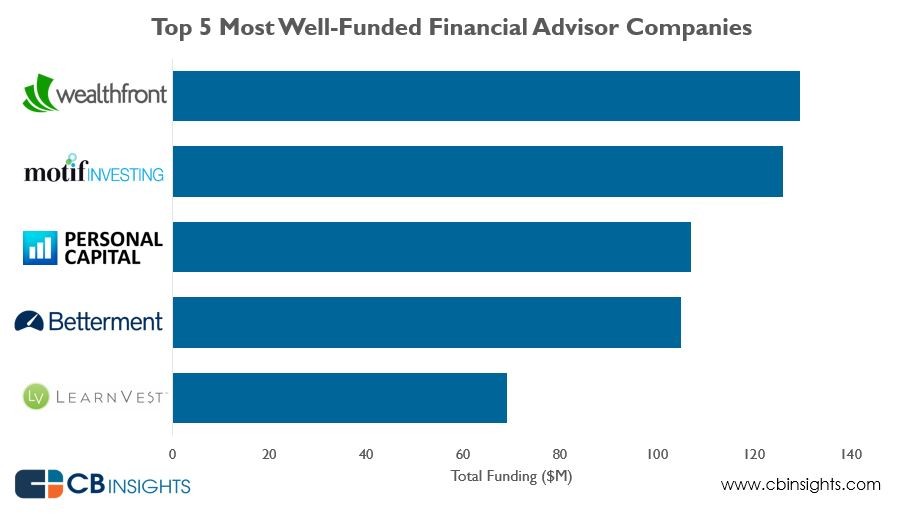

Popular robo-advisors for your investment needs

It all started with Betterment, the online investment company based in New York City. Today, they have over $7.3 billion in AUM. From automatic rebalancing, handling diversified portfolios, tax-loss harvesting to managing your IRA, the robo-advisors will be at your disposal for all your financial needs. We list a few companies who are offering customized computer-generated advice.

Now, it is interesting to watch that robo-advisors, which started off in the US are now finding major support in different parts of the world. The market of automated investing is growing at an exponential pace and major players from different countries are increasingly becoming a part of this FinTech journey. From Switzerland, UK to Asia-Pacific (APAC) region, the rising popularity of robo-advisors can be felt in the financial space.

As indicated by BI Intelligence, the APAC region will represent $2.4 trillion in robo advisor AUM by 2020.Also, clients across all asset classes are interested in robo-advisors, including the opulent class. According to BI Intelligence, 49% of high-net-worth individuals i.e. HNWIs across the world would consider having a robo advisor manage at least some portions of their money.

BI also indicated that by 2020, 60% of these HNWIs would invest 20% of their assets in robo-advisors.In most cases, robo-advisors are considered to be the economical way to invest in contrast to traditional wealth management firms.

Agreed, there are challenges for both robo-advisors and traditional firms, which rely on human advisors, to acquire customer base and modulate strategy respectively. So, let’s wait and watch how more investors respond to the new arrangement.

Reference: Fox Business, CB Insights, USA Today, Wall Street Journal, invstr, Forbes, Business Insider, Mint, Economic Times