We're building something new – take a look at the beta site: intglobal.com

The alarming worldwide increase in Sandboxing usage has been the consequence of the mushrooming of FinTech companies. This has led to the establishment of regulatory sandboxing by financial regulatory body establishing a medium where FinTechs can experiment and test innovative products, services, business models and delivery mechanisms in a live market with real consumers. This has been with the major objective of instilling an optimal balance between ensuring financial stability and consumer protection while also enabling beneficial innovation.

A Global Overview

The launch of ‘Project Innovate’ in 2014, the UK’s Financial Conduct Authority has won recognition for the success of its sandbox. It has paved the way for major compliances in different nations and building trust across regulatory institutes of why they should consider having a sandbox.

Since then a number of nations have introduced and improved the framework.

Financial Conduct Authority’s report, Lessons Learned provides a firsthand experience of the first 6 month cohorts of 50 firms of which 41 FinTechs successfully tested their products in a regulatory framework. Some successful sandboxing examples-

Sandboxing: Need For The Indian Ecosystem

According to KPMG, the Fintech market is set to reach USD 2.4 billion by 2020 which is double its worth of 2016 that stood at USD 1.2 billion. The innovative breakthrough by FinTechs has given rise to major data security challenges which leapfrogged with the prevalent use of Open Banking system that provides a user with a network of financial institutions’ data. Open Banking has been a boon for FinTechs like PayTm, PayU who have already successfully incorporated APIs to share information, but has definitely raised eyebrows.

Source: Pwc

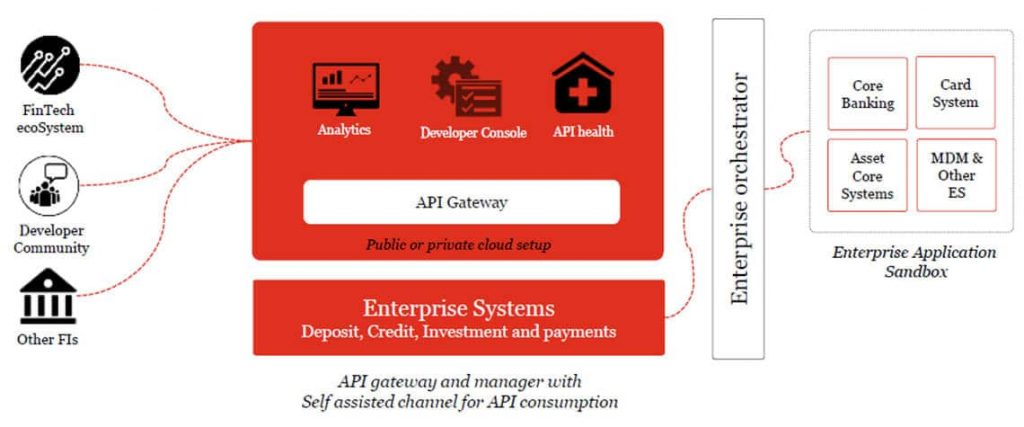

As APIs are gaining traction it is only recently that firms have begun to step up to secure their online spaces as consumers are getting aware of threats such as phishing –which not only threaten a customer’s main bank account but also all their other chosen financial providers. Drawing examples from the worldwide success of regulatory sandboxing, RBI has proposed a Regulatory Sandbox where businesses can test innovative products under relaxed conditions.

Salient Features of RBI’s Regulatory Sandboxing

The focus of Regulatory Sandboxing is being on thematic cohorts such as financial inclusion, payments and lending, digital KYC; any product/services which have been banned by the regulators or the government, including cryptocurrency/crypto assets services, have strictly been discouraged.

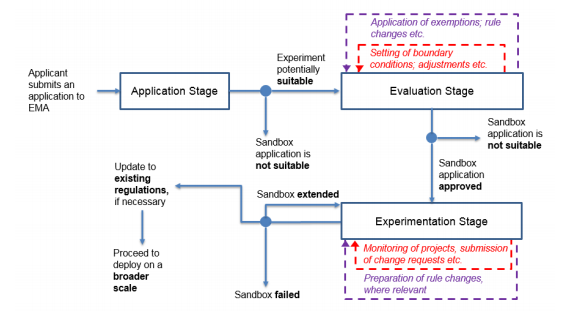

Source: EMA

What Can Organizations Expect?

Currently, more than 400 FinTechs are operating in the country and their investments are expected to grow by 170% by 2020. Regulatory Sandboxing comes as an encouragement for digital disruptors like us to develop and explore innovative products and services. FinTechs need to streamline decision-making processes to improve agility and partnering with digital solution providers will enable your company to deploy sandboxing methodologies to fastrack your processes.