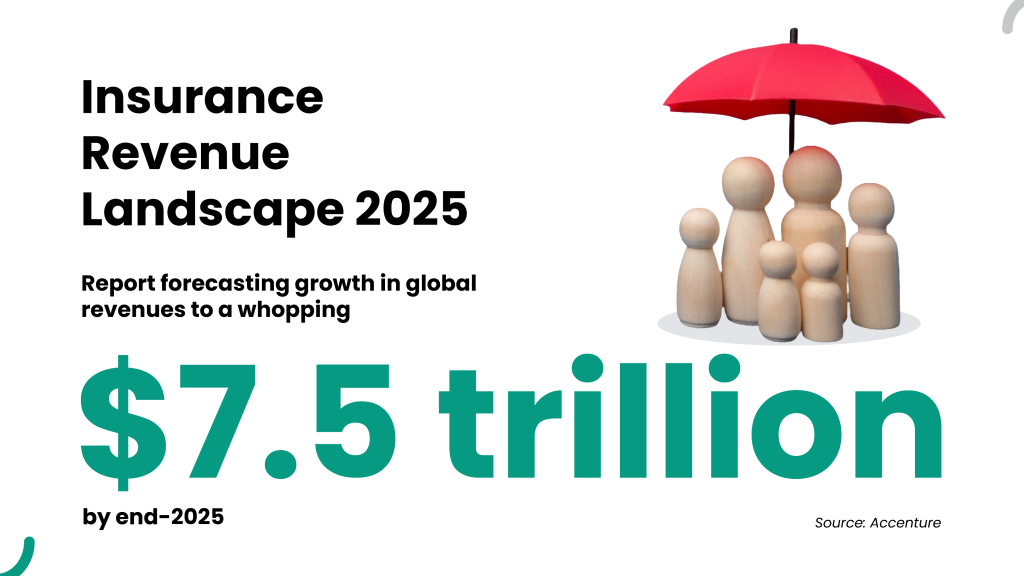

InsureTech is the latest buzzword that is making the headlines in the insurance sector and with good reason. From suitable risk assessment using alternate data to tapping big data analytics and artificial intelligence in insurance for better outcomes in diverse arenas, insurers are expected to step on the gas further across the next couple of years in this domain. Here is a brief glimpse into the same.

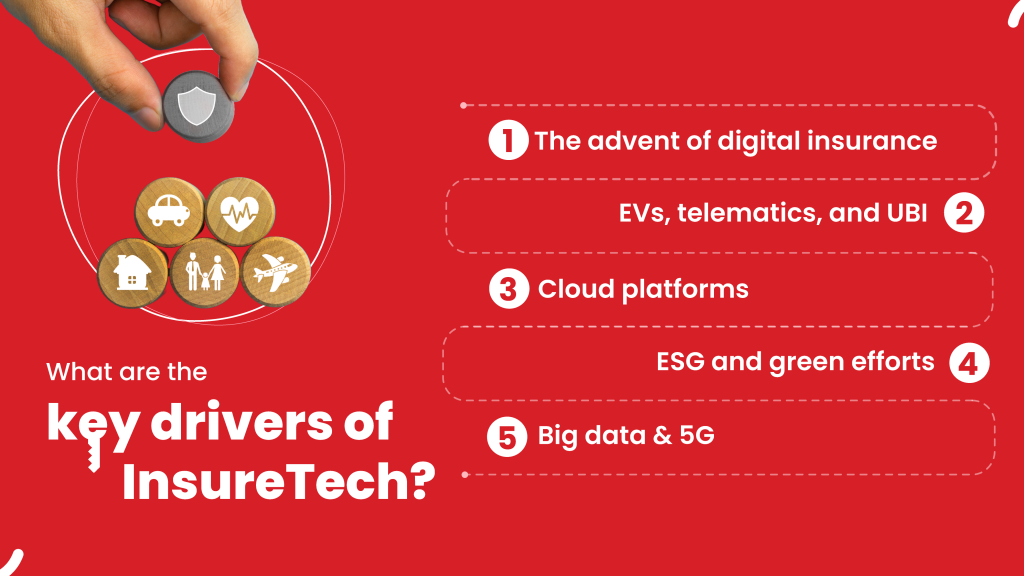

1.What are the key drivers of InsureTech?

The advent of digital insurance- Legacy systems are slowly on their way out, with digital offerings becoming commoner. Reports by CB Insights and Gallagher Re have already stated how InsureTech entities have drawn US$15.8 billion and counting in investments over the last year and are swiftly scaling up due to the same.

EVs, telematics, and UBI- Usage-based insurance (UBI) coverage driven by big data analytics and artificial intelligence in insurance are key trends that are propelling the growth of InsureTech at multiple levels. Add to this coverage for the gig economy, private customers, fleets, and more. The electric mobility market is also on the cusp of growth and market-driven products and services based on telematics and other data are already gaining ground as a result.

Cloud platforms: Digital players are leveraging cloud services for data applications, storage, and scalability, replacing on-site systems.

ESG and green efforts: InsureTech players are actively investing in ESG regulations and forming sustainable partnerships with like-minded investors. This attracts customers who align with these goals, and ESG guidelines help with risk assessment and management.

Big data and 5G: The global 5G rollout improves connectivity and provides more data sources for insights. Insurance companies utilize KYC-driven insights and big data analytics to gain valuable information. They also leverage alternative data for enhanced risk assessment and mitigation.

These are some of the major driving forces behind the InsureTech revolution that is sweeping the world today. Let us now learn a little more about the deployment of artificial intelligence in insurance.

Artificial intelligence in insurance and InsureTech are symbiotically linked due to the multifarious applications and use cases that have transformed the industry in recent years. Here are a few aspects worth noting in this regard:

AI is enabling better processing of claims, with machine learning automating various tasks to eliminate errors and lower claims processing timelines considerably.

This data can be integrated into underwriting for better risk assessment, claims processing, and decision-making with lower risks.

NLP (natural language processing) is helping insurance companies evaluate risks through several alternate data channels or abstract resources.

Case acceptance ratios are not only increasing, but there is a reduction in underwriting time as well.

With the insurance industry losing sizable revenues to fraud every year, AI has completely changed the game for them. Systems are now smart enough to identify repeated or suspicious patterns and flag instances that need immediate attention.

AI is also enabling better reporting of insurance claims with easy assigning, triage, routing, and facilitation.

Chatbots are also taking care of customer communication, while AI is streamlining all the other procedures like authorisation, data capturing, tracking payments, and approvals.

AI is also boosting better operational efficiencies, faster customer responses, automation of repetitive processes, and better up-selling or cross-selling of products/services tailored to customer requirements.

Improved loss estimation is another key facet of leveraging artificial intelligence in insurance.

AI is beneficial for the entire InsureTech ecosystem in multiple ways, as is mentioned above. A closer look is also necessary at the various sources or types of alternate data that insurance companies can use for better risk assessment.

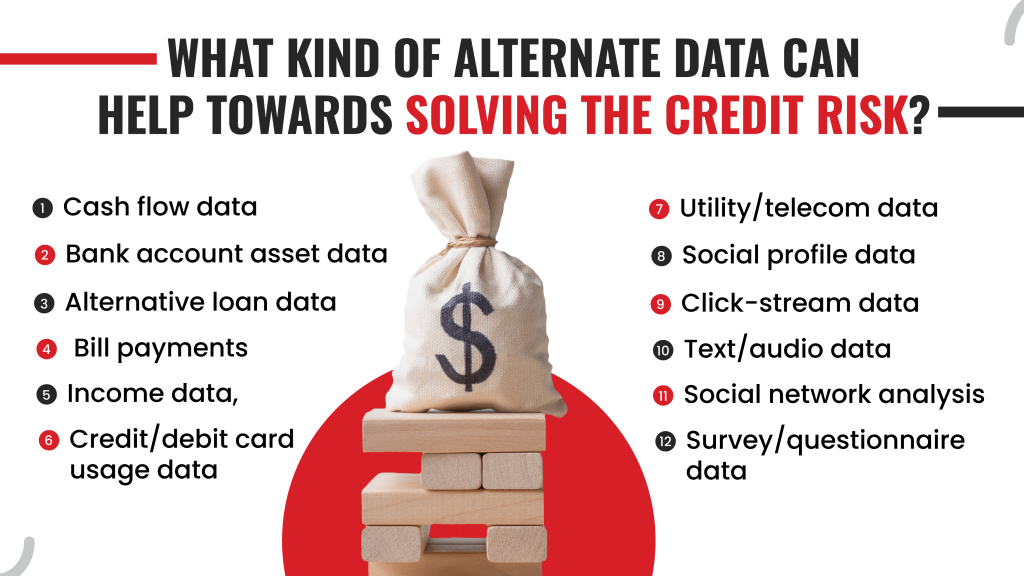

3.What kind of alternate data can help towards solving the credit risk?

Cash flow data- This includes account information and inflows/outflows of money. This can be used to work out spending and income patterns for determining eligibility.

Bill payments for utilities, rent, phone, insurance, and other aspects for determining the creditworthiness of a customer.

Alternative loan data including BNPL (buy now pay later) and paycheck advances can also be gathered.

Rental or home loan payment data.

Data on bank account assets including current, pending, and historic account balances.

Income data through payrolls and other sources of information.

Usage of credit or debit cards, ratios of spends and cash to total spends, and so on.

Utility, telecom, and other data including social profile data, click-stream data, text and audio data, social network analysis, etc.

Survey or questionnaire data can also be used by insurance companies for this purpose.

FAQs

1.What are the privacy and ethical considerations associated with using alternate data in risk assessment for InsureTech?

InsureTech players must address privacy, ethics, and data validity when using alternate data. Key considerations include responsible data collection and usage, obtaining consent, ensuring analytical tool validity, fairness, and unbiased systems, data quality, regulatory compliance, and full disclosure principles.

2.Are there any successful case studies or real-world examples of InsureTech companies leveraging alternate data for risk assessment?

There are many examples of InsureTech entities making use of alternate data for risk assessments. ZestFinance, for instance, deploys AI for evaluating both traditional and non-traditional information to gauge risks while automating its underwriting procedure for lower risks. Nauto has already been using AI for forecasting purposes. The aim here is to avoid collisions of commercial fleets (driverless) by lowering distracted driving. The AI system uses data from the vehicle, camera, and other sources to predict risky behavior.

3. What future trends do you foresee in the use of alternate data for risk assessment in the InsureTech industry?

There will be greater emphasis on leveraging telematics and usage data garnered through connected vehicles and IoT devices along with smart home devices. At the same time, more machine learning models will be used for algorithm-based risk assessments. The Metaverse will be another channel for insurers to combine their AI-backed Chatbots with sales pitches, internal training, data gathering, and even NFTs for personal document verification.

4. Are there any challenges or limitations in leveraging alternate data for risk assessment in InsureTech?

There are a few limitations/challenges in using alternate data for assessing risks in the InsureTech space. The quality of the data and whether it tells the whole story is one challenge along with the fact that there are ethical and privacy-related considerations, regulatory aspects, and the issues related to disclosures, user consent, and the methods of gathering data.

Summary

Article Name

InsureTech Insights: Leveraging Alternate Data for Risk Assessment

Description

Leveraging alternative data for insurance risk assessment: Unlocking valuable insights and improving accuracy