Blockchain continues to be a talking point throughout various sectors, including insurance. From insurance underwriting and risk management to fraud prevention, it has several applications that promise to change the future of insurance.

This technology not only guarantees data integrity through its immutable smart contracts, but also promises to usher in higher transparency at multiple levels.

The key take-away here is that Blockchain helps build higher trust amongst parties for information-sharing. This is encrypted as an electronic records list or blocks which cannot be tampered or erased. Smart contracts are digitally-signed and computable agreements between parties.

They enable information sharing and execution in a secure way. Let us look at how Blockchain has a major impact on insurance underwriting and other functions like risk management.

Blockchain for Decentralised Insurance

Blockchain applications in the insurance sector are increasingly being explored by several companies. With Web 3.0 and DeFi setting new process and system standards throughout various sectors, insurance is no exception. Here are a few points worth noting in this regard:

Decentralised insurance enables more decentralised and easier access to conventional insurance services.

Decentralised insurance focuses on enabling decentralised access to insurance policies.

This approach enables better claims management. Instead of scrutinising damages for finalising payouts, parameter-based insurance may offer faster processes. Parametric insurance may help in finalising payouts after checking for compliance with policy-defined insurance parameters.

Smart contracts can be used for parametric insurance contracts and their usage within DeFi (decentralised finance) protocols may generate higher value.

Self-executing contracts may enable better policy management with lower fees and conflicts resulting from claims management and insurance processes.

These insurance protocols offer higher security due to Blockchain’s immutable nature.

Decentralised insurance thus makes the whole process faster and more reliable.

Decentralised insurance may help access patient-linked data on the Blockchain with full consent and automated data verification, secure storage, and zero tampering.

Blockchain may be helpful in not only accessing but also managing innumerable transactions while enabling automatic record collection. It may also link information across sources as smart contract inputs to take better decisions.

Fraud detection and risk management are also enhanced with Blockchain technology. Smart contracts can be used for verifying claim authenticity and referring to multiple records.

Customer experiences will improve with decentralised insurance models, speedier claims processing, and interoperable and complete data records. It will boost insurance underwriting, helping complete it in minutes. Insurance companies can also get verified and secure policyholder data for updating records.

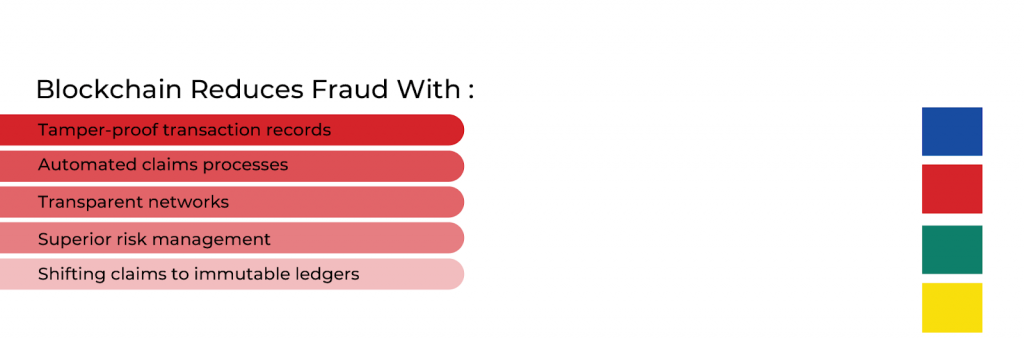

How blockchain can reduce fraud

Can Blockchain reduce fraud? Here are some pointers that are worth looking at in this regard:

Blockchain technology can lower fraud through the creation of tamper-proof transaction records.

Smart contracts can readily automate claims processes, thereby leading to quicker fraud detection and lowering fraud possibilities altogether. Fraudulent claims can be quickly identified as a result.

Through the development of a more transparent and secure network, Blockchain will boost trust between customers and insurance companies.

Smart contracts will ensure superior risk management too. Decentralised insurance algorithms will take care of the entire process, enabling the policy set-up in quick time.

Through shifting insurance claims to immutable ledgers, common fraud sources will be eliminated throughout the insurance sector.

Blockchain is not only helpful for fraud detection and decentralisation in insurance, but also for ensuring improved regulatory compliance.

Blockchain for regulatory compliance

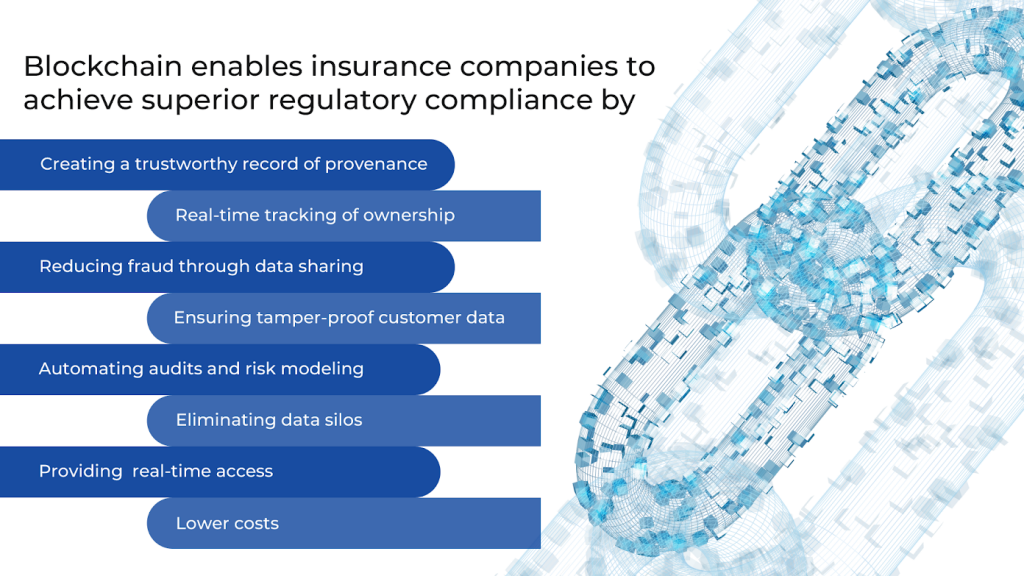

There is a leading role played by Blockchain technology in helping insurance companies enable superior regulatory compliance across the board. Here’s how:

It can build a trustworthy and immutable record of provenance for stakeholders.

It can track ownership of products and insurance claims on a real-time basis across locations.

It can boost claims fraud reduction with improved data sharing.

It can build a customer data repository that cannot be tampered, while enabling smooth data sharing across companies.

It lowers duplication and risk errors through its operational dynamics, while enabling higher customer visibility throughout institutions.

It works to boost regulatory compliance while minimising oversights.

It can also automate audits, compliance checks, and risk modeling while building treaties and risk towers upon time-stamped and single smart contracts.

It can eliminate data silos, giving customers full consent and higher control over their data, inclusive of rights of access.

Maintaining vital regulatory information and regulations on a Blockchain network enables easier and immutable access along with higher visibility into compliance-related activities.

The technology can also help regulatory agencies monitor the steps needed for implementing various regulations. They can get real-time access to compliance data securely on the Blockchains of regulated insurance entities.

This helps them stay updated, while lowering effort, time, and costs greatly.

FAQs

1.How blockchain can streamline claims processing?

Blockchain technology can enable real-time information access for all parties. This helps reduce conflicts and disputes, thereby enabling faster claims processing and payouts.

2.How blockchain can improve customer satisfaction?

Blockchain technology can enhance customer satisfaction in the insurance industry due to its impact on faster and streamlined claims management. Claims can be processed swiftly without conflicts or delays. This naturally improves customer satisfaction greatly.

3.The challenges of implementing blockchain in insurance?

Some of the challenges involved in implementing Blockchain in the insurance industry include technological integration into legacy systems and the absence of regulatory frameworks for several applications.

4. The future of blockchain in insurance

Blockchain will shape the future of the insurance industry in a major way. Smart contracts and securely-held policyholder data will be the norm. Digital evidence required for underwriting will be provided by the Blockchain, while enabling higher data control and consent for customers. Underwriting and claims management will be automated and more efficient as a result. Fraud detection will also be enhanced with immutable and secure transaction records.

Summary

Article Name

Blockchain's Impact on Risk Management

Description

Explore how blockchain revolutionizes risk management. Discover advanced solutions for secure, transparent, and efficient risk assessment and mitigation.