We're building something new – take a look at the beta site: intglobal.com

Risk and youth go hand in hand. If you are thinking we are talking about thrill-seeking and adventurous youngsters, then here’s the clarification. We are talking about youth and their ability to take the risk in investment. Yes, you read that right.

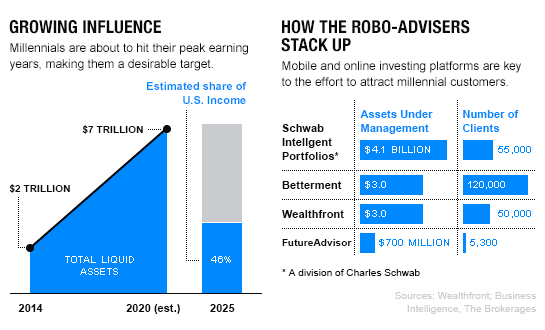

It’s this risk taking and digitally active generation, which is gradually re-shaping the FinTech sector. As indicated by Wealthfront, millennials will control $7 trillion in liquid assets by 2019.

That is surely quite an achievement.

The financial institutions are adopting technological innovations such as machine learning, big data and artificial intelligence (AI) to engage and retain digitally-savvy young investors. The robo-advisors, the latest FinTech innovations, are finding followers in millennials. Studies and research suggest that young investors are willing to rely on robo-advisors more than human financial advisors.

The use of robo-advisors, thanks to the advancement in AI in FinTech is set to explore more in the coming days. These algorithm-based advisors cater to the needs of digitally motivated customers, thus helping companies and also investors make cheaper, faster and better decisions.

Did you know Wealthfront, one of the leading robo-advisors, has resulted in the growth of AUM from $100 million to over $3.7 billion by September 2016, placing it in the top 100 independent registered investment advisors in the United States?

The advent of robo-advisors has definitely given a much-needed boost to the existing business models in the FinTech world especially when it comes to portfolio management, asset management, wealth management and financial planning. So, let’s take a quick look at how robo-advisors can help the millennials and also the retirees.

Robo-advisors and millennials

Let’s admit it. Young guns have changed the way we bank and invest. They don’t prefer to visit the bank physically. Face-to-face business meetings, endless waiting at banks, and filling out numerous yet similar forms are passé. Millennials want everything fast and want to control all their finances and investments at their fingertips via smart devices or computers.

This is where robo-advisors are scoring over financial advisors. Millennials prefer handling banking and investing services online. Working with robo-advisors is less time-consuming and require less of paperwork too. These automated investment services offer an easy interface, which is comfortable to use. Millennials like that.

Robo-advisors are a great choice for young investors who require portfolio management for a specific savings goal. In that case, the young investor need not worry about other aspects of wealth management such as retirement planning. Also, according to the financial climatic condition, the algorithms reshape the portfolio of the investors.

Credit: Sachs Insights

According to Meir Statman, professor of behavioural finance at Santa Clara University, automation is important to attract youngsters to invest and adopt good savings habits early on.

An individual financial advisor or advisory firm charge 1 % or higher. Here’s the catch. Robo-advisors are economical.

For small investors, finding a good financial advisor might come at a cost. And taking help of agents for important financial service and investment decisions are not always a worthy advice. In such initial cases, robo-advisors can come handy and build a portfolio at a lesser cost than a human advisor, who comes at a higher cost.

According to Wealthfront, financial advisors charge 1.31% average fee. However, a robo-advisor charges an annual fee of 0.25% and 0.50%. Betterment, one of the pioneer robo-advisers, charges 0.15%-0.35%. According to a report by Business Insider, a robo-adviser SigFig charges $10 every month.

Robo-advisers are good for people who are interested in Exchange-Traded Fund (ETFs) and they are a low-cost solution. Robo-advisors make the process of investing faster and easier. Both Betterment and Wealthfront charge management fee of 0.15% per year for ETFs.

Millennials are a very profitable section of the market, comprising 25% of the US population and 21% of consumer discretionary purchases. Knowing how to reach them is vital for survival in today’s market, especially if you’re a company or product that is tied to the technology field.

Also, let’s not forget how millennials love their freedom, be it in life or money matters. This is where robo-advisors score again. These automated investment platforms encourage the investors to manage the portfolio on their own (read DIY) by asking them about risk tolerance and investment model they want to choose. Accordingly, the computer algorithms will decide a portfolio for you.

According to an article in CNBC, Wealthfront also looks after millennials and their early focus was on young “techies” in the Silicon Valley.

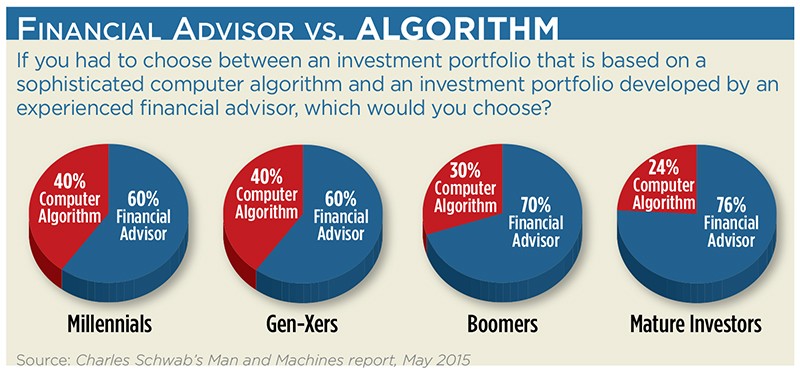

Take a quick glance at some of the reasons why millennial find robo-advisors interesting:

Robo-advisors and baby boomers

Can a retiree who has considerable assets to invest and wealth to preserve rely on a computer for investment planning? Well, even a few years ago, most of the answers to this question would have been an absolute ‘no’. But technology has changed a lot in our lives. And it has also changed our mindset.

Today, retirees or baby boomers or the silent generation are no longer hesitant towards adopting technological innovations. Agreed, though most retirees prefer having a human advisor who will manage investment portfolio and provide tailor-made financial advice as and when the market moves, with each passing day, baby boomers are also trying out these computer algorithms for their financial planning.

Take this: According to an article published in January 2017 in Business Insider, nearly half of Schwab’s Intelligent Portfolio consumers are above the age of 50. Also, approximately two-thirds of Vanguard’s Personal Advisor Service customers are approaching the age of retirement age or have already retired.

We are all aware that baby boomers, pre, and post retirees have more wealth than the young investors. This means people above the age of 50 have a greater volume of assets under management (AUM).

True Link, a California-based financial service firm, launched robo-advisory services for retirees and those approaching retirement.

According to an article published in Forbes, Kai Stinchcombe, founder and CEO of True Link was quoted as saying, “Our strategy has been to get really good at understanding retired people and then build products based on our knowledge of that demo.”

The same article mentioned how Dream Forward Financial, a startup for 401(k) investors, is providing computerized emotional advice for employees of all ages.

Did you know Betterment retirement robo division has attracted nearly 300 companies to 401(k) platform within a few months?

Now, before going for a robo-advisor, it’s important to consider the kind of investment one wants to make. Most of the existing robo-advisors today help in choosing ETFs with lower expense ratios. However, at times, retirement planning can be a complicated issue and in this case, robo-advisors might not always be fruitful. Also, a retiree or people nearing retirement are critical about their future investment and planning. They are not risk takers or embracers like the millennials. Rather, they are risk avoiders.

They want a financial advisor with experience on tax efficiency and retirement drawdown advice, who has weathered much market vitality and can provide worthy advice. Also, a retiree likes to study the market before making a decision regarding money, hence he or she might not be in a hurry to invest.

Retirees are also concerned about the security of sharing sensitive information online without any human intervention.

And though robo-advisors can handle tax loss harvesting and other tax-advantaged strategies, there may be at times when human intervention is needed to handle a critical situation.

In the case of market volatility or personal moments affecting investment, a retiree does not like a DIY model. He wants an expert advice and will prefer approaching a human adviser. In simple terms: he would likely want a personal human touch rather than a computerized version.

Advantages of robo-advisors

Disadvantages of robo-advisors

Conclusion

Without a doubt, robo-advisors are one of the exhilarating advancements in technology in the financial sector in recent times. The services provided by these automated investment platforms are growing with each day. That, however, doesn’t mean that robo- advisors are fast replacing human advisors. However, the growing demand of these algorithms based advisors obviously indicates that they will cast a major impact in the financial advisory space in the next few years. Also, industry experts believe that with time, robo-advisors will become wholesome financial advisors and not just portfolio managers.

According to entrepreneur Steven Van Belleghem, investment is about predicting what will happen in the future and AI-enabled robo-advisors are all about that. A big believer in robo advisors, Belleghem also authored the book, “When Digital Becomes Human”, which received the award for ‘Best Marketing Book of 2015’.

The race between the machines and humans has started. Let’s see who wins the race.